GENERAL

SFM Club: The Ultimate Guide to Benefits, Features, and More

The SFM Club has gained significant attention as a platform offering financial education, networking opportunities, and business tools for aspiring entrepreneurs. Whether you’re looking to build passive income, learn digital marketing, or connect with like-minded individuals, understanding what the SFM Club offers can help you make an informed decision. This guide explores its features, benefits, and how it compares to similar platforms, ensuring you have all the details before joining.

What Is the SFM Club?

The SFM Club (Six Figure Mentors Club) is a membership-based community designed to help individuals achieve financial freedom through online business education. Founded by industry experts, it provides training programs, mentorship, and resources to help members build and scale digital businesses. Unlike generic courses, the SFM Club focuses on actionable strategies, including affiliate marketing, e-commerce, and lead generation.

Key Features of the SFM Club

-

Comprehensive Training Modules – Step-by-step guides on digital marketing, sales funnels, and automation.

-

Expert Mentorship – Access to experienced entrepreneurs who provide personalized guidance.

-

Community Support – A global network of members for collaboration and motivation.

-

Scalable Business Models – Strategies that adapt whether you’re a beginner or advanced marketer.

-

Tools & Resources – Pre-built templates, software discounts, and automation tools.

How Does the SFM Club Work?

Joining the SFM Club grants you immediate access to its training portal, live webinars, and private forums. The program is structured into phases, starting with foundational lessons and progressing to advanced techniques. Members can interact with mentors, ask questions, and receive feedback on their business strategies. Additionally, the club frequently updates its content to reflect the latest industry trends.

Who Should Join the SFM Club?

-

Aspiring entrepreneurs seeking structured training.

-

Freelancers or professionals wanting to transition into online business.

-

Existing business owners looking to scale using digital strategies.

-

Individuals interested in passive income streams like affiliate marketing.

SFM Club vs. Alternatives: A Detailed Comparison

To help you evaluate whether the SFM Club is the right fit, here’s a comparison table highlighting five key aspects:

| Feature | SFM Club | Competitor A | Competitor B |

|---|---|---|---|

| Cost | Mid-range membership fee | Higher pricing tiers | Free with limited access |

| Efficiency | Structured, step-by-step | Self-paced but less guided | Overwhelming for beginners |

| Ease of Use | User-friendly dashboard | Complex navigation | Simple but lacks depth |

| Scalability | Focused on long-term growth | Short-term tactics | Limited advanced strategies |

| Benefits | Mentorship + community | Solo learning | Basic tutorials only |

As seen, the SFM Club balances affordability with structured learning, making it ideal for those who want mentorship alongside practical training.

Pros and Cons of the SFM Club

Advantages

-

Hands-on training – No fluff, just actionable steps.

-

Supportive community – Reduces the isolation often felt in online business.

-

Proven strategies – Focuses on methods that work in real-world scenarios.

Potential Drawbacks

-

Membership cost – May be a barrier for some beginners.

-

Time commitment – Success requires consistent effort.

-

Niche focus – Primarily for digital marketing and affiliate-based models.

Is the SFM Club Worth It?

If you’re serious about building an online business, the SFM Club offers a clear roadmap. The mentorship and community aspects set it apart from free courses, providing accountability and expert insights. However, it’s not a “get-rich-quick” scheme—real results come from applying the strategies consistently.

Final Thoughts on the SFM Club

The SFM Club stands out as a structured platform for those committed to building an online business. With expert mentorship, a supportive community, and scalable strategies, it provides real value for entrepreneurs willing to put in the work. Before joining, assess your goals and budget to ensure it aligns with your needs.

FAQs

What is the cost of joining the SFM Club?

The SFM Club operates on a membership basis, with pricing tiers depending on the level of access. While exact figures may vary, it’s positioned as a mid-range investment compared to other business training programs.

Can beginners succeed with the SFM Club?

Absolutely. The training is designed to take members from the basics to advanced strategies, making it beginner-friendly while still valuable for experienced marketers.

Does the SFM Club guarantee income?

No legitimate program can guarantee income, and the SFM Club is no exception. Success depends on effort, consistency, and applying the taught strategies effectively.

Are there any hidden fees?

The membership fee covers core training, but additional tools or upsells may be optional. Always review terms before committing.

How active is the SFM Club community?

The community is highly active, with regular updates, live Q&A sessions, and member interactions to foster growth and networking.

Is the SFM Club a pyramid scheme?

No. The SFM Club focuses on education and digital business strategies rather than recruitment-based earnings, differentiating it from pyramid schemes.

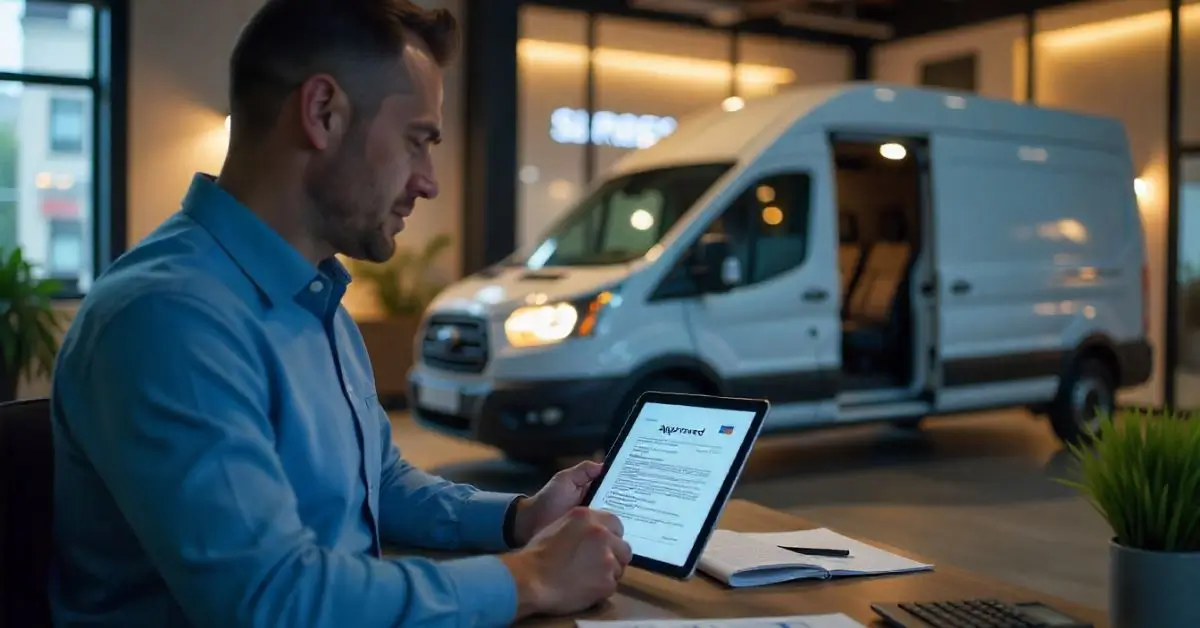

Every growing business needs reliable transportation, and business auto loans provide the financial flexibility to acquire vehicles without straining cash flow. Whether you’re a small business owner expanding your fleet or a corporation upgrading to fuel-efficient models, understanding how these loans work can save you time and money. This guide covers everything from loan types and eligibility to expert tips for securing the best rates—helping you make an informed decision for your company’s needs.

How Business Auto Loans Work

Business auto loans are specialized financing options designed to help companies purchase vehicles for commercial use. Unlike personal auto loans, these are tailored to business needs, offering higher borrowing limits, flexible repayment terms, and potential tax benefits. Lenders evaluate your creditworthiness, business revenue, and the vehicle’s purpose before approving the loan.

Types of Business Auto Loans

-

Term Loans – A lump-sum amount repaid over a fixed period with interest. Ideal for businesses with strong credit.

-

Equipment Financing – The vehicle serves as collateral, often resulting in lower rates.

-

Commercial Leasing – Businesses “rent” the vehicle for a set term, with options to buy afterward.

-

SBA Loans – Government-backed loans with competitive rates for eligible small businesses.

Key Benefits of Business Auto Loans

Investing in a business auto loan offers several advantages:

-

Preserved Cash Flow – Avoid large upfront payments and allocate capital to other operational needs.

-

Tax Deductions – Interest payments and depreciation may qualify as business expenses.

-

Improved Credit Profile – Timely repayments can strengthen your business credit score.

-

Fleet Expansion – Scale your operations without financial strain.

However, failing to secure favorable terms can lead to higher costs, so comparing lenders is crucial.

Eligibility Requirements

Lenders assess multiple factors before approving a business auto loan:

-

Credit Score – A strong personal or business credit score (680+) increases approval odds.

-

Business Revenue – Proof of consistent income reassures lenders of repayment capability.

-

Down Payment – Typically 10%–20% of the vehicle’s price.

-

Business Age – Older businesses (2+ years) often qualify for better rates.

Startups or businesses with poor credit may need to explore alternative lenders or offer collateral.

Comparing Business Auto Loan Options

To help you evaluate lenders, here’s a comparison of five key features:

| Feature | Banks | Credit Unions | Online Lenders | Dealership Financing | SBA Loans |

|---|---|---|---|---|---|

| Interest Rates | Low | Competitive | Moderate-High | Varies | Lowest |

| Approval Speed | Slow | Moderate | Fast | Instant | Slow |

| Eligibility | Strict | Moderate | Lenient | Flexible | Strict |

| Loan Terms | 3–7 yrs | 2–6 yrs | 1–5 yrs | 2–5 yrs | Up to 10 yrs |

| Down Payment | 10–20% | 5–15% | 0–15% | 0–10% | 10–30% |

Banks and SBA loans offer the best rates but require strong credentials, while online lenders provide quicker access at higher costs.

Tips for Securing the Best Business Auto Loan

-

Check Your Credit – Review your business and personal credit reports for errors.

-

Compare Multiple Lenders – Rates and terms vary significantly.

-

Negotiate Terms – Use competing offers as leverage.

-

Consider Total Costs – Include insurance, maintenance, and fuel in your budget.

-

Pre-Approval Advantage – Strengthens your position when dealing with dealerships.

Avoid long-term loans with excessive interest, as they can inflate the total cost unnecessarily.

Common Pitfalls to Avoid

-

Overborrowing – Purchase only what your business needs.

-

Ignoring Fees – Origination fees, prepayment penalties, and late charges add up.

-

Skipping Gap Insurance – Covers the difference if the vehicle is totaled and the loan isn’t fully paid.

-

Rushing the Process – Hasty decisions lead to unfavorable terms.

Final Thoughts

Business auto loans are a powerful tool for companies seeking to acquire vehicles without depleting working capital. By understanding loan types, eligibility, and lender comparisons, you can secure financing that aligns with your business goals. Always prioritize transparency, compare offers, and plan for long-term affordability to maximize the benefits.

FAQs

What’s the difference between a business auto loan and a personal auto loan?

Business auto loans are designed for commercial use, offering higher loan amounts, tax benefits, and flexible terms tailored to companies. Personal loans are based on individual credit and lack these advantages.

Can startups qualify for business auto loans?

Yes, but options may be limited. Startups might need a strong personal credit score, collateral, or a larger down payment to secure approval.

Are interest payments on business auto loans tax-deductible?

In most cases, yes. The IRS allows businesses to deduct interest expenses on loans used for operational assets like vehicles. Consult a tax professional for specifics.

How long does it take to get approved?

Traditional banks may take weeks, while online lenders or dealership financing can approve loans within hours or days.

What’s better: leasing or buying with a loan?

Leasing offers lower monthly payments and flexibility, while buying builds equity and offers long-term savings. Evaluate your business’s cash flow and vehicle needs.

Can I refinance a business auto loan?

Absolutely. Refinancing can lower interest rates or monthly payments if your credit or market conditions improve.

Managing business expenses efficiently is crucial for growth, and the PNC Bank Business Credit Card offers a powerful solution. Designed to streamline cash flow, simplify tracking, and reward spending, this card helps businesses of all sizes optimize their financial operations. Whether you’re a small business owner or manage a larger enterprise, understanding the benefits, features, and potential drawbacks of this card can help you make an informed decision.

Why Choose the PNC Bank Business Credit Card?

A business credit card is more than just a payment tool—it’s a financial management asset. The PNC Bank Business Credit Card stands out with competitive rewards, expense management tools, and flexible payment options. Here’s why it could be the right fit for your business:

1. Rewards and Cash Back

Earn points or cash back on every purchase, helping offset costs. Many cards offer higher rewards in key spending categories like office supplies, travel, or gas—ideal for businesses with frequent expenses in these areas.

2. Expense Tracking and Reporting

Simplify bookkeeping with detailed monthly statements and customizable reports. Some cards integrate with accounting software, reducing manual entry errors and saving time.

3. Employee Spending Controls

Issue cards to employees while setting individual spending limits. This minimizes misuse and ensures budgets stay on track.

4. No Personal Liability Protection

Unlike personal credit cards, some business cards don’t hold owners personally liable for unpaid balances—though terms vary.

5. Introductory APR Offers

Take advantage of low or 0% APR promotions to finance large purchases or manage cash flow during slower months.

Comparing the PNC Bank Business Credit Card to Competitors

To help you evaluate whether this card meets your needs, here’s a comparison of five key features:

| Feature | PNC Bank Business Credit Card | Competitor A | Competitor B | Competitor C |

|---|---|---|---|---|

| Annual Fee | Low or waived first year | Moderate | High | None |

| Rewards Rate | Up to 1.5% cash back | 1% flat | 2% on select categories | 1.25% |

| Employee Cards | Free with spending controls | Fee applies | Limited controls | Free but no controls |

| APR | Competitive variable rate | Higher rate | Low intro APR | Standard rate |

| Expense Tools | Advanced reporting | Basic | Integrates with accounting software | Minimal |

This table highlights how the PNC Bank Business Credit Card balances cost, rewards, and functionality, making it a strong contender for businesses prioritizing flexibility and control.

How to Apply for a PNC Bank Business Credit Card

Applying is straightforward, but approval depends on your business’s financial health. Follow these steps:

1. Check Eligibility Requirements

Most issuers require a good personal credit score (670+), a registered business, and proof of revenue.

2. Gather Necessary Documents

Prepare tax IDs, financial statements, and personal identification before applying.

3. Submit Your Application

Apply online or at a PNC branch. Approval can take minutes or a few days, depending on verification needs.

4. Activate and Start Using

Once approved, activate your card and enroll in online banking to monitor transactions.

Potential Drawbacks to Consider

While the PNC Bank Business Credit Card offers many advantages, it’s important to weigh potential downsides:

-

Variable APR After Intro Period – If you carry a balance, interest costs can add up quickly.

-

Rewards Redemption Limits – Some programs restrict how or when you redeem points.

-

Personal Guarantee Requirement – Many business cards require a personal credit check, which could impact your score if mismanaged.

Maximizing Your Card’s Benefits

To get the most from your PNC Bank Business Credit Card, follow these best practices:

-

Pay On Time – Avoid late fees and interest by setting up autopay.

-

Monitor Spending – Review statements monthly to detect fraud or overspending.

-

Leverage Rewards – Use points for travel, statement credits, or reinvestment in your business.

-

Negotiate Fees – Some issuers waive annual fees if you ask, especially with strong spending history.

Final Thoughts

The PNC Bank Business Credit Card provides a robust financial tool for businesses seeking rewards, spending controls, and expense management. By understanding its features, costs, and best-use strategies, you can decide if it aligns with your company’s needs.

FAQs

What credit score is needed for a PNC Bank Business Credit Card?

A FICO score of 670 or higher is typically required, though some cards may demand a stronger credit profile for premium rewards.

Does the PNC Bank Business Credit Card report to personal credit bureaus?

Most business cards report delinquencies to personal bureaus but not routine activity—check terms to confirm.

Can I get employee cards for free?

Yes, PNC offers complimentary employee cards with customizable spending limits.

Is there a 0% introductory APR offer?

Some PNC cards include introductory 0% APR periods, usually lasting 6–12 months.

How do I redeem cash back rewards?

Rewards can typically be redeemed as statement credits, checks, or deposits into a PNC account.

What happens if I miss a payment?

Late payments may incur fees and penalty APRs, and could harm your credit score if reported.

Planning a trip across the Mississippi River? The Belle Chasse Ferry schedule is essential for commuters, tourists, and locals alike. Whether you’re heading to work, exploring Louisiana’s scenic routes, or transporting goods, knowing the ferry’s operating hours, frequency, and potential delays ensures a stress-free journey. This guide covers everything you need—from real-time updates to cost comparisons—helping you navigate the ferry system with confidence.

Why the Belle Chasse Ferry Matters

The Belle Chasse Ferry is a vital transportation link connecting Plaquemines Parish to the West Bank of New Orleans. Unlike congested bridges, the ferry offers a relaxing alternative with picturesque river views. However, unexpected schedule changes or long waits can disrupt travel plans, making it crucial to stay informed.

Key Benefits of Using the Belle Chasse Ferry

-

Avoids traffic bottlenecks on major bridges.

-

Cost-effective compared to toll routes.

-

Scenic experience with views of the Mississippi River.

Belle Chasse Ferry Schedule: Operating Hours and Frequency

The Belle Chasse Ferry schedule typically runs daily, but exact timings vary. Here’s what to expect:

Weekday Schedule

-

First departure: 5:00 AM (East Bank to West Bank)

-

Last departure: 9:00 PM (West Bank to East Bank)

-

Frequency: Every 20–30 minutes during peak hours (6:00 AM–8:30 AM and 4:00 PM–6:30 PM).

Weekend and Holiday Schedule

-

First departure: 6:30 AM

-

Last departure: 8:30 PM

-

Frequency: Every 45 minutes.

Note: Schedules may shift due to weather, maintenance, or emergencies. Always check for updates before heading out.

How Weather Affects the Belle Chasse Ferry Schedule

Heavy fog, high winds, or storms can suspend operations temporarily. In extreme cases, the ferry may halt service for hours or even a full day. If you’re traveling during hurricane season (June–November), monitor local advisories closely.

Comparing the Belle Chasse Ferry to Alternative Routes

To help you decide whether the ferry suits your needs, here’s a comparison of five key features:

| Feature | Belle Chasse Ferry | Crescent City Connection Bridge | Harvey Tunnel |

|---|---|---|---|

| Cost | Free | $1–$2 (toll) | Free |

| Efficiency | Moderate (wait times) | Fast (unless congested) | Fast |

| Ease of Use | Simple boarding | Subject to traffic jams | Narrow lanes |

| Scalability | Limited capacity | Handles high volume | Moderate |

| Benefits | Scenic, no tolls | Reliable in fair weather | Quick access |

Tips for a Hassle-Free Ferry Experience

-

Arrive Early: Boarding queues can form quickly during rush hour.

-

Check Real-Time Updates: Follow local transit alerts for delays.

-

Prepare for Weather: Bring sunscreen in summer or an umbrella in rain.

-

Know the Alternatives: Have a backup route in case of cancellations.

What to Do If the Ferry Is Delayed

Delays happen—mechanical issues, high traffic, or weather disruptions can extend wait times. If you’re on a tight schedule, consider the Crescent City Connection Bridge or carpooling to reduce stress.

Future Improvements to the Belle Chasse Ferry System

Officials have discussed modernizing the ferry fleet and increasing frequency to meet growing demand. While no official timeline exists, upgrades could reduce wait times and improve reliability.

Final Thoughts

The Belle Chasse Ferry schedule is a lifeline for many, offering a convenient and scenic way to cross the Mississippi. By planning ahead and staying updated, you can avoid delays and enjoy a smooth trip. Whether you’re a daily commuter or a first-time visitor, this guide ensures you’re prepared for every possibility.

FAQs

How Often Does the Belle Chasse Ferry Run?

The ferry operates every 20–30 minutes on weekdays and every 45 minutes on weekends. Peak hours see more frequent departures.

Is the Belle Chasse Ferry Free?

Yes, the ferry is currently toll-free for all vehicles and pedestrians.

What Time Does the Last Ferry Leave?

The last weekday departure is at 9:00 PM, while weekends end at 8:30 PM.

Can I Walk onto the Belle Chasse Ferry?

Absolutely! Pedestrians and cyclists are welcome without additional fees.

Does the Ferry Operate During Mardi Gras?

Yes, but schedules may adjust for parades and events. Verify timings in advance.

What Happens If I Miss the Last Ferry?

You’ll need to use an alternate route like the Crescent City Connection Bridge or arrange overnight accommodations.

-

GENERAL8 months ago

GENERAL8 months agoDoge 5000 Check: What It Is and Why It Matters

-

ENTERTAINMENT8 months ago

ENTERTAINMENT8 months agoVirginia Tech Football News: Latest Updates, Key Insights, and Future Outlook

-

TECHNOLOGY8 months ago

TECHNOLOGY8 months agoBroadviewNet: The Ultimate Solution for Reliable and Scalable Connectivity

-

TECHNOLOGY9 months ago

TECHNOLOGY9 months agoSlimyim Regretevator: A Game-Changer in Adaptive Feedback Loops

-

TECHNOLOGY7 months ago

TECHNOLOGY7 months agoHow a Med Tech Certificate Can Launch Your Career

-

GENERAL8 months ago

GENERAL8 months agoAnne Dias: A Trailblazer in Finance and Philanthropy

-

GENERAL8 months ago

GENERAL8 months agoCoomer Party: The Ultimate Guide to Understanding the Trend

-

GENERAL8 months ago

GENERAL8 months agoWelll: Benefits, Features, and Practical Insights